Where Should I Invest $2,000 Right Now?

I originally wrote this article in 2021 during COVID, when stimulus checks were plentiful. Given the recent announcement by POTUS that he wants to provide working families (but not high earners) with $2,000 stimulus checks, I felt the urge to revisit this article.

Alright, so you just got ahold of $2,000—what do you do with it next?

Honestly, putting it into your emergency fund so that you have at least 3–6 months’ worth of expenses saved is probably the right move. If your emergency fund is good to go, an ETF or mutual fund that tracks the S&P 500 is your next best option.

I remember when I got my first stimulus check in 2020 and invested it into Bitcoin. I’ve sold some of the Bitcoin along the way, but it’s amazing what “free money” invested into funny internet money became. In fact, had you invested your $1,200 stimulus check in 2020 into Bitcoin and not sold, you would have had around $21,000 at the beginning of October 2025. Of course, you would have been down quite a bit at certain points along the way, but a gain of 1,701% in five years is staggering.

Now to the point of this article. Since my emergency fund has enough money to cover three months of expenses, here’s where I would invest my hypothetical $2,000 stimulus check:

#1: Investing in ETFs

My favorite method for long-term investing is purchasing shares in an ETF that tracks the S&P 500. Owning shares in one of these ETFs allows you to own a small portion of the 500 largest U.S. companies.

ETFs often have lower expense ratios compared to mutual funds, which is one reason why I prefer them. Below is a list of ETFs that track the S&P 500 index:

Vanguard S&P 500 ETF (VOO)

Expense Ratio: 0.03%

Annual Dividend Yield: 1.09%

Assets Under Management: $1.6 trillion

SPDR S&P 500 ETF (SPY)

Expense Ratio: 0.09%

Annual Dividend Yield: 1.07%

Assets Under Management: $681 billion

iShares Core S&P 500 ETF (IVV)

Expense Ratio: 0.03%

Annual Dividend Yield: 1.04%

Assets Under Management: $705 billion

I personally invest in VOO, but any of the above three are excellent options and should serve as a cornerstone of any long-term portfolio.

#2: Investing in Individual Stocks

Another great way to invest $2,000 is in individual stocks. Investing in companies you like and that have strong fundamentals can pay off greatly in the long run. However, investing in individual stocks always carries more risk compared to investing in ETFs, because a stock can ultimately go to zero.

Individual stocks will either beat the market, match the market’s return, or perform worse than the market average. Making a list of companies you regularly shop at, hold in high regard, or have had great experiences with is a good place to start when identifying potential investments.

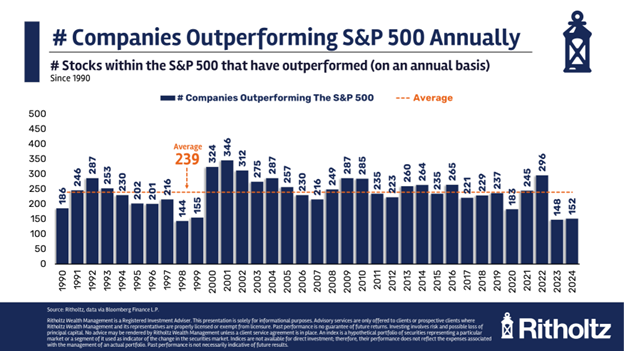

This chart is really interesting. Historically, in any given year, there is slightly less than a 50% chance that an individual stock will outperform the S&P 500. Over longer periods—such as 5-, 10-, or 15-year intervals—that percentage decreases significantly.

That said, individual stocks are how outsized gains are made. For example, in the last five years, Nvidia is up 1,231%. A $2,000 investment in Nvidia five years ago would be worth $24,620 today. On the flip side, Lyft is down 46% over the same period. A $2,000 investment in Lyft five years ago would be worth $1,080. Ouch.

#3: Investing in Certificates of Deposit (CDs)

For individuals who prefer a less risky and more conservative option, purchasing a Certificate of Deposit (CD) is a great choice. CDs, which can be purchased at your bank or through your broker, lock up your money for a specific period of time and pay you interest during that period.

For example, a 12-month $1,000 CD with a 2% interest rate will pay $20 in total interest over the life of the CD. At maturity, your original $1,000 is returned to you along with the earned interest.

CD interest rates are fixed, and CDs are federally insured up to $250,000. This means that if the financial institution issuing your CD fails, the federal government will reimburse you for your lost funds, up to the insured limit.

CD rates generally move with broader interest rate trends and vary depending on Federal Reserve policy. Longer-term CDs typically offer higher interest rates than shorter-term CDs. While CDs may not provide high returns, they are an excellent way to preserve capital and earn predictable income, especially during uncertain market conditions.

#4: Investing in Yourself

Truthfully, this option should probably be listed first.

I firmly believe in investing in yourself—whether that’s your mental health, physical health, spiritual well-being, learning a new skill, taking an online class, or simply doing something that recharges your batteries.

We can all improve at something, and your new hobby might even lead to an additional income stream or help make you indispensable at work.

The website https://www.classcentral.com offers a wide range of free online classes covering topics such as coding, artificial intelligence, history, languages, career development, and more.

Investing in your health is always important, especially during stressful or uncertain times. Healthy eating, regular exercise, and activities like reading or yoga can reduce stress and improve overall well-being. Purchasing equipment for home workouts, learning to cook healthy meals, or participating in virtual activities with friends and family can all be done affordably and contribute to a better quality of life.

Recent Articles I’ve Read:

3 Great International ETFs for 2026 and Beyond (Zachary Evens)

CD Rate Forecast: Are CD Rates Going Up in 2026? (Spencer Tierney)

Why You (and I) Need a Career Coach (Kevin Hall)

Is Home Equity Fake Wealth? (Nick Maggiulli)

Disclaimer: This blog is for informational and educational purposes only and reflects the personal opinions of the author. It does not constitute financial, investment, tax, or legal advice. The views expressed are solely those of the author and do not represent the views of Rising Wealth Financial Services LLC. Rising Wealth Financial Services LLC does not provide investment advisory services. Readers should consult a qualified professional before making any financial or investment decisions.